The Balanced Scorecard (BSC) is a strategic management framework introduced by Robert S. Kaplan and David P. Norton in the early 1990s. It is designed to translate an organization’s strategy into a set of balanced performance measures across different perspectives. The BSC goes beyond financial metrics to include non-financial indicators, providing a more comprehensive view of organizational performance. The four key perspectives in the Balanced Scorecard are Financial, Customer, Internal Business Processes, and Learning and Growth.

-

1. Financial Perspective:

Financial perspective focuses on financial performance metrics that indicate the organization’s success in achieving its financial objectives and creating value for shareholders. It helps organizations assess their financial health and performance in terms of shareholder value.

Examples: Revenue growth, profit margins, cost reduction, return on investment, cash flow.

-

Customer Perspective:

Customer perspective concentrates on customer-related metrics to assess how well the organization is meeting customer expectations and delivering value. Organisations define key customer metrics to understand how well they are meeting customer needs and expectations.

Examples: Customer satisfaction, market share, customer retention, brand perception.

-

Internal Business Processes Perspective:

This perspective evaluates the efficiency and effectiveness of internal processes that contribute to delivering value to customers and achieving financial goals. It identifies critical processes and measures efficiency, quality, innovation, and other factors that contribute to organizational success.

Examples: Process cycle time, quality metrics, cost efficiency, innovation.

-

Learning and Growth Perspective:

This perspective focuses on the organization’s ability to innovate, learn, and grow to support long-term success. The metrics may include employee training, skill development, and technology infrastructure to ensure long-term sustainability.

Examples: Employee training and development, employee satisfaction, innovation and creativity, organizational culture.

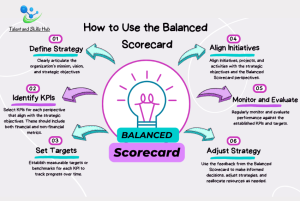

How to Use the Balanced Scorecard:

-

Define Strategy:

Clearly articulate the organization’s mission, vision, and strategic objectives.

-

Identify Key Performance Indicators (KPIs):

Select KPIs for each perspective that align with the strategic objectives. These should include both financial and non-financial metrics.

-

Set Targets:

Establish measurable targets or benchmarks for each KPI to track progress over time.

-

Align Initiatives:

Align initiatives, projects, and activities with the strategic objectives and the Balanced Scorecard perspectives.

-

Monitor and Evaluate:

Regularly monitor and evaluate performance against the established KPIs and targets.

-

Adjust Strategy:

Use the feedback from the Balanced Scorecard to make informed decisions, adjust strategies, and reallocate resources as needed.

WATCH THE VIDEO HERE>>>

Balanced Scorecard Example:

Let’s consider an example of a software development company:

-

Financial Perspective:

KPI: Revenue Growth Rate

Target: Achieve a 15% increase in revenue over the next fiscal year.

-

Customer Perspective:

KPI: Customer Satisfaction Index

Target: Maintain a satisfaction index of 85% or higher based on customer surveys.

-

Internal Business Processes Perspective:

KPI: Development Cycle Time

Target: Reduce the average development cycle time by 20% through process optimization.

-

Learning and Growth Perspective:

KPI: Employee Certification Rate

Target: Increase the percentage of certified employees by 15% through training programs.

Benefits of the Balanced Scorecard:

- Holistic View: Provides a balanced and comprehensive view of organizational performance.

- Alignment: Aligns day-to-day activities with the overall strategic objectives.

- Communication: Facilitates communication and understanding of the strategy across the organization.

- Continuous Improvement: Promotes continuous improvement by focusing on key areas of importance.

Limitations of Balanced Scorecard

-

Complexity and Implementation Challenges:

The BSC, with its multiple perspectives and numerous performance indicators, can be complex to design, implement, and maintain. Organizations may face challenges in defining meaningful metrics and ensuring that the entire workforce understands and embraces the framework.

-

Overemphasis on Quantifiable Metrics:

The BSC often focuses on quantifiable metrics, which may not fully capture the complexity of certain strategic objectives. As a result, qualitative aspects, such as organizational culture or employee morale, may be overlooked.

-

Potential for Information Overload:

Attempting to track too many metrics across various perspectives can lead to information overload. Decision-makers may struggle to identify the most critical indicators, and the excessive volume of data may hinder effective decision-making.

-

Static Nature of Measurement:

The BSC typically involves setting targets for specific time periods. However, this static nature can be a limitation, as it may not capture the dynamic and evolving nature of some strategic goals. Real-time adjustments may be necessary but are not always accommodated.

-

Subjectivity in Measurement:

Some performance indicators, especially in the customer and learning perspectives, can be subjective and open to interpretation. This subjectivity may lead to biases and challenges in consistent measurement.

-

Limited Focus on External Factors:

The BSC primarily concentrates on internal factors and may not adequately address external influences such as changes in the competitive landscape, economic conditions, or regulatory environments.

-

Potential for Short-Term Focus:

Organizations might become overly focused on short-term objectives and financial outcomes, neglecting longer-term strategic goals. This is especially true if there is a heavy emphasis on financial metrics.

-

Resistance to Change:

Implementing the BSC may face resistance from employees who are accustomed to traditional performance measurement systems. The shift toward a more balanced and holistic approach may encounter resistance, requiring a cultural shift within the organization.

-

Cost and Resource Intensity:

Developing and maintaining a Balanced Scorecard system can be resource-intensive in terms of time, costs, and technology requirements. Smaller organizations or those with limited resources may find it challenging to implement the BSC effectively.

-

Not a One-Size-Fits-All Solution:

The BSC may not be suitable for every organization or industry. The appropriateness of the framework depends on the organization’s size, industry, and the nature of its strategic objectives.

Despite these limitations, the Balanced Scorecard remains a valuable tool for many organizations when used thoughtfully and adapted to fit their specific needs and circumstances. Organizations should be aware of these limitations and make informed decisions about whether the BSC is the right strategic management framework for them.

Final Remark.

The Balanced Scorecard has been widely adopted across industries and sectors as a strategic management tool to enhance performance measurement and decision-making. It helps organizations move beyond a sole focus on financial metrics and consider a broader set of factors that contribute to sustained success.